TL;DR

- Transfer pricing is the mechanism that sets prices for every transaction between related entities in your group

- The OECD recognizes five methods for pricing intercompany transactions, and the right choice depends on your transaction type, data availability, and comparability

- In 2026, compliance means navigating Pillar Two, AI-driven audit selection, and tightening documentation deadlines

- Implementation requires mapping all intercompany transactions, selecting the right method, documenting everything contemporaneously, and building a monitoring process that keeps executed prices within approved bands

- Vistaar's SmartPricing Suite gives manufacturing and CPG enterprises a centralized, rules-based engine to manage internal transfer pricing alongside commercial pricing

An estimated 44% of all US imports and exports in 2024 moved between related parties within the same corporate group, according to US Census Bureau data.

When you operate across multiple entities, transfer pricing is not a background function. It determines how margin moves across your plants and divisions, what your P&Ls actually reflect, and how exposed you are when a tax authority comes knocking.

Get it wrong, and you face double taxation, regulatory penalties, and months of litigation. Get it right, and it becomes a lever for operational clarity and defensible profit allocation.

This guide covers what transfer pricing is, the five OECD-recognized methods, how to implement it, what compliance entails, and how pricing software like Vistaar eliminates the manual burden of managing intercompany prices across entities and jurisdictions.

What is Transfer Pricing?

Transfer pricing is the way a company prices transactions between its own related entities, including goods, services, and royalties. These intercompany prices directly determine how revenue and costs are allocated across entities, which in turn shapes each entity's taxable income in its jurisdiction.

This pricing strategy applies to cross-border transactions between subsidiaries in different countries and to domestic intercompany transactions between divisions or business units.

Transfer pricing is a legal, regulated discipline. The risk of non-compliance comes from setting prices that deviate from market rates without proper documentation. When pricing is inconsistent, undocumented, or disconnected from operational reality, it attracts scrutiny; but when it follows a defensible methodology, it does not.

The arm's length principle

The arm's length principle (ALP) requires that transactions between related entities be priced as if they were conducted between independent, unrelated parties under comparable conditions. It is the global standard for assessing whether an intercompany price complies.

The ALP is codified in Article 9 of the OECD Model Tax Convention and detailed in the OECD Transfer Pricing Guidelines, used by over 140 countries. In the US, Section 482 of the Internal Revenue Code establishes the same standard for IRS enforcement purposes.

The principle exists to prevent artificial profit shifting. Without it, a multinational could set transfer prices to concentrate income in low-tax jurisdictions and strip taxable profits from high-tax ones. The ALP ensures each jurisdiction collects tax on income that reflects genuine economic activity.

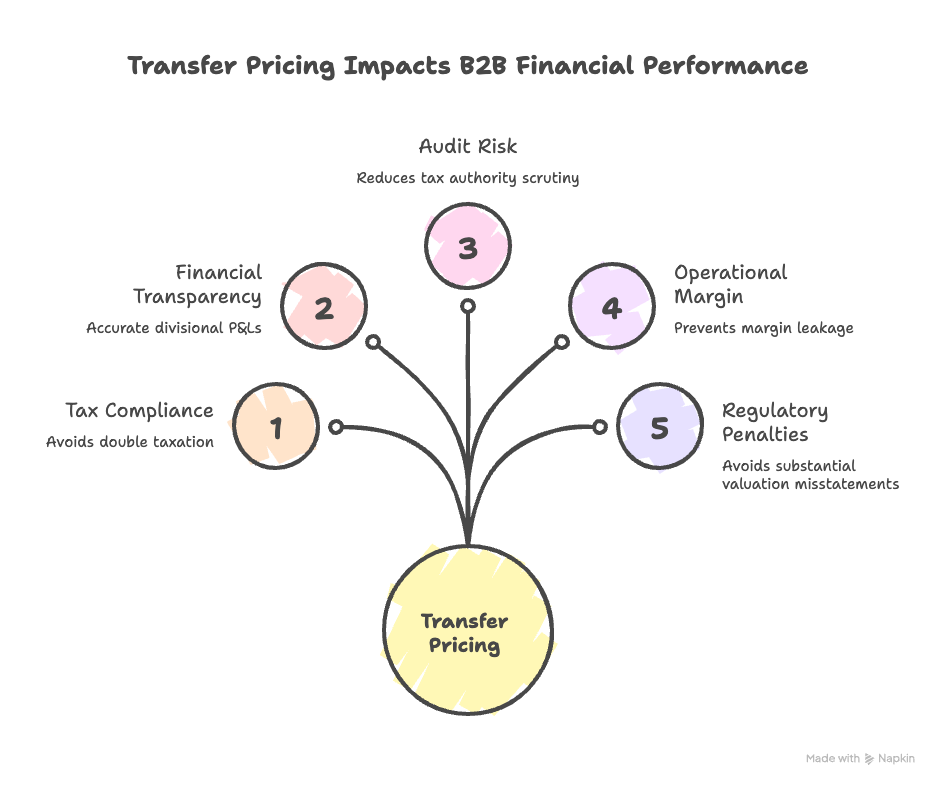

Why Transfer Pricing Matters for B2B Enterprises

Transfer pricing touches every dimension of multi-entity financial performance. It shapes internal cost structures, divisional investment cases, and how accurately leadership can read where the business is making money.

Here is what is at stake across five dimensions:

- Tax compliance and avoiding double taxation: Incorrect transfer prices can result in the same income being taxed in two jurisdictions. Proper transfer pricing, supported by OECD guidelines and bilateral tax treaties, prevents this

- Financial transparency and accurate reporting: Transfer prices feed directly into divisional P&Ls. Set them arbitrarily, and you distort internal performance metrics, mislead decision-making, and create misaligned incentives between plants and distribution entities

- Audit risk reduction: Tax authorities globally are intensifying scrutiny. The OECD published updated transfer pricing country profiles in July 2025, and Pillar Two (the global minimum tax) adds new layers of complexity

- Operational margin impact: The transfer price between a production plant and its distribution arm determines each entity's margin. When this price is set by a spreadsheet or habit rather than methodology, margin leakage is inevitable

- Regulatory penalties: Deloitte's 2024 global transfer pricing survey found that penalties are now common or automatic in nearly 75% of countries. In the US, IRC Section 6662 allows penalties of up to 40% for substantial valuation misstatements

The 5 Core Transfer Pricing Methods

The OECD recognizes five transfer pricing methods, grouped into traditional transaction methods and transactional profit methods. You must apply the best method rule to choose the most reliable arm’s length result for your data and transaction type.

1. Comparable uncontrolled price (CUP) method

CUP compares the price in your controlled transaction to a comparable transaction between independent parties under similar conditions. It is the most direct method and is preferred when reliable market comparables exist.

CUP works best for commodities, raw materials, and financial transactions where external market prices are publicly observable. It becomes difficult when product specifications or contractual terms differ between the controlled and uncontrolled transactions.

Example: A manufacturer sells steel components to its distribution subsidiary at $50 per unit. An identical sale to an unrelated buyer in the same quarter is also $50 per unit. That match confirms the transfer price is arm's length.

2. Resale price method

The resale price method starts with the price at which a product is sold to an independent customer, then subtracts an appropriate gross margin to arrive at the arm's length transfer price. It is best suited for distribution and resale scenarios where the distributor performs routine functions and holds no unique intangibles.

Example: A consumer goods distributor purchases products from its parent at $40 per unit and resells them to retailers at $65/unit. If comparable independent distributors earn a 35% gross margin, the arm's length transfer price works out to approximately $42.25/unit.

3. Cost plus method

Cost plus adds an arm's length markup to the producer's or service provider's total cost base. It is common in contract manufacturing, intra-group services, and R&D arrangements.

The main risk is inconsistency in cost accounting: if different entities apply different cost treatment, your benchmark becomes unreliable and harder to defend.

Example: A contract manufacturing subsidiary incurs a total cost of $30/unit. A 15% markup, consistent with comparable contract manufacturers, sets the arm's length transfer price at $34.50/unit.

Also Read: Effective Pricing Analysis: Models, Methods, and Tools That Protect Margin

4. Transactional net margin method (TNMM)

TNMM compares the net profit margin generated by the controlled transaction with that of comparable independent companies, measured against an appropriate base such as costs, sales, or assets.

It is the most widely used method across industries because it works even when detailed transaction-level comparables are unavailable.

Example: A distribution subsidiary earns a net margin of 4% on sales. Benchmarking against comparable independent distributors shows an arm's-length range of 3% to 6%. The subsidiary's margin falls within that range, confirming compliance.

5. Profit split method

The profit split method allocates combined profits or losses between related entities based on each entity's relative contribution, measured by functions performed, assets employed, and risks assumed.

It is used when transactions are so integrated that they cannot be evaluated in isolation, common in IP-heavy industries, digital platforms, and highly integrated supply chains.

Under the 2025 OECD Amount B framework, a simplified margin range of 1.5% to 5.5% applies to baseline distribution activities, reducing the benchmarking burden for qualifying routine distributors.

Example: A parent company develops proprietary software and licenses it to a manufacturing subsidiary that uses it to improve production yields. Both entities contribute meaningfully to value creation.

The profit split method allocates combined profits based on each entity's R&D spend, headcount, and operational contribution rather than benchmarking a single transaction.

How to Implement Transfer Pricing Effectively

Implementing transfer pricing is an operational discipline that requires clear ownership, method selection grounded in your transaction reality, and ongoing monitoring. The following four steps map the process from first principles to audit readiness.

Step 1: Map all intercompany transactions

Start by cataloguing every flow of goods, services, royalties, IP, and financing between related entities, including internal service fees like shared IT, legal, and HR that are often buried in overhead. Classify each transaction as tangible goods, services, IP, or financial instruments, since this drives eligible methods, documentation needs, and implicated tax jurisdictions.

Because transfer pricing documentation spans tax, finance, pricing, and local controllers, start by defining a clear Responsible, Accountable, Consulted, and Informed (RACI) model, then select your method:

- Who sets transfer prices

- Who approves methodology changes

- Who updates benchmarking annually

- Who signs off on documentation

For a concrete example of how structured pricing disciplines play out in a complex B2B environment, see our guide to pricing strategies in the steel industry.

Step 2: Select the appropriate method

Apply the best method rule. Three factors determine which method produces the most reliable arm's length result:

- Transaction type narrows your options fast. Distribution points to the CUP or resale price. Contract manufacturing fits cost plus. Integrated transactions with shared IP typically land on TNMM or profit split

- Data availability decides what's viable in practice. CUP demands transaction-level comparables, which are often hard to find. TNMM works at the entity level, which is why it's the most widely used method across industries

- Comparability determines how much you can defend. The more adjustments your comparables need, the weaker your position under scrutiny

Once your method is set, keep your benchmarks up to date. Reusing last year's comparable set without verification is one of the most common triggers for transfer pricing adjustments.

Refresh annually, or after any material change: new product lines, supply chain restructures, or shifts in how functions and risks are allocated. If your comparables are more than two to three years old, update before your next filing.

Step 3: Set prices and document everything

Once you select a method, calculate the transfer price and document the analysis contemporaneously at the time of the transaction.

Under the OECD’s three-tier framework, you must maintain a Master File (group overview and policies), a Local File (entity-level analysis and benchmarking), and a CbCR for groups above the revenue threshold.

However, Germany’s 2025 changes go further by mandating the automatic submission of key documents. That includes the Master File, a new Transaction Matrix, and extraordinary transaction documentation within 30 days of a tax audit notice, with the Local File due within 30 days if specifically requested.

Clearly document your method rationale: why this method over alternatives, what comparables you used, any comparability adjustments, and the arm’s length range or price, because vague or incomplete rationale is treated much like no documentation in many jurisdictions.

Step 4: Monitor, audit-proof, and adjust

Transfer pricing is not set-and-forget. Each of the three actions in this step serves a distinct purpose.

Monitor means reviewing your benchmarks and executed prices on a regular basis.

Check the intercompany prices in your order system with your approved transfer pricing policy. When they drift, the gap between what your documentation says and what your ERP executes is exactly what AI-driven audit tools are built to find.

Audit-proof means building your defence before scrutiny arrives, not scrambling after an audit notice. Practically, that looks like:

- Maintaining contemporaneous documentation updated to reflect current business conditions

- Locking in methodology for high-risk or high-volume transactions through Advance Pricing Agreements (APAs)

- Keeping intercompany agreements current so that contractual terms reflect the economic substance of how entities operate

Adjust means responding to change before it creates a compliance gap. Any material shift in your business warrants a transfer pricing review:

- New product lines or supply chain restructures

- Significant input cost movements or FX shifts

- Changes in how functions, assets, or risks are allocated between entities

When prices change, brief regional leaders and finance teams beforehand to ensure the change takes effect. Explain the new calculation, the arm's length range, and the entity-level margin impact.

Advantages and Disadvantages of Transfer Pricing

Transfer pricing is not purely a compliance cost. Managed well, it gives you accurate divisional P&Ls, reduces double taxation risk, and creates a defensible audit position.

Understanding both sides helps you build the internal business case, set realistic expectations with finance and tax stakeholders, and decide where software or external expertise reduces the burden enough to make the investment worthwhile.

Transfer Pricing Compliance: What You Need to Know in 2026

The 2026 compliance environment is the most demanding it has ever been. OECD updates, Pillar Two rollout, IRS enforcement expansion, and AI-driven audit selection are converging into a higher-scrutiny environment for every enterprise with intercompany transactions.

Documentation requirements

The three-tier OECD framework (Master File, Local File, CbCR) is now the baseline in virtually every jurisdiction with active transfer pricing rules. Documentation must be contemporaneous, meaning prepared at the time intercompany transactions are entered into.

Key thresholds vary by jurisdiction, but for most enterprises with cross-border intercompany transactions and consolidated group revenue above EUR 750 million, CbCR filing is mandatory. Below that threshold, Local File and Master File requirements still apply in most OECD-aligned jurisdictions, often with lower revenue thresholds set at the local level.

Penalties and audit risk

The scale of exposure is not hypothetical. The IRS's long-running dispute with Coca-Cola over royalty pricing reached a critical point in late 2024 when the company paid a $6 billion deposit to stop interest accrual while it appeals a potential $18 billion total liability.

Similarly, Meta faced a multi-billion-dollar challenge over 2010 IP valuations; while a May 2025 Tax Court decision reduced the IRS's $20 billion claim, it still affirmed a significant $7.8 billion adjustment.

For B2B enterprises, these cases make one thing clear: thin documentation and ad‑hoc transfer prices now carry real exposure to adjustments, penalties, and protracted disputes.

What matters in 2026 is having a defensible methodology that matches how you do business, real‑time controls to keep executed prices within arm’s‑length bands, and a single system of record that can stand up to a data‑driven audit.

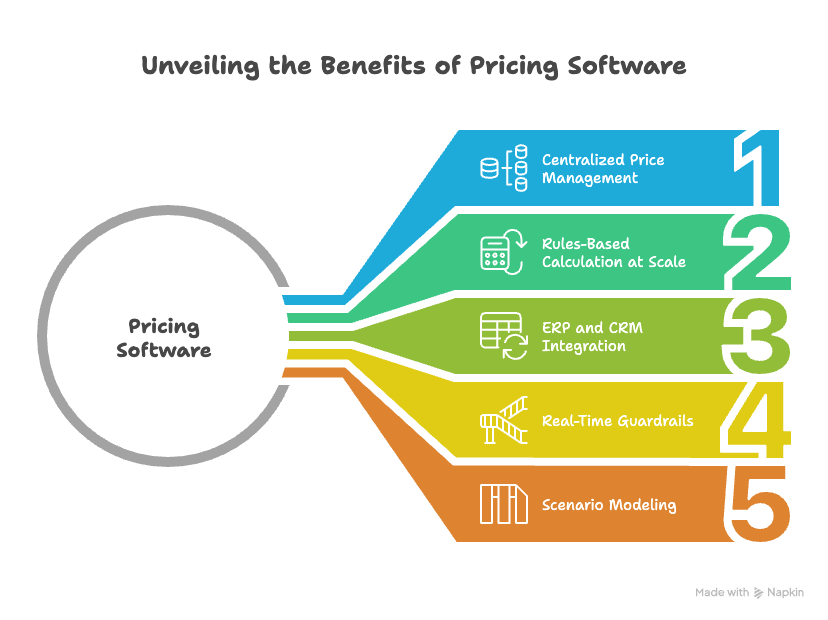

How Pricing Software Simplifies Transfer Pricing Management

Most enterprises still manage intercompany pricing in disconnected spreadsheets. This leads to three issues: no real-time view of true entity-level margins, weeks of manual effort to update prices when rules or costs change, and silent drift between approved and executed transfer prices.

Dedicated pricing software addresses each of these problems directly:

- Centralized price management: A single platform holds transfer prices, commercial prices, rebate structures, and discount policies together, giving you a unified view of entity- and deal-level margin

- Rules-based calculation at scale: Cost-plus, margin-based, and TNMM-aligned calculations run automatically when input costs, exchange rates, or product mix changes, without manual spreadsheet intervention

- ERP and CRM integration: API connections ensure that approved transfer prices flow directly into order processing, financial reporting, and downstream settlement systems, eliminating the manual handoff where drift occurs

- Real-time guardrails: Price execution rules enforce approved transfer price bands. Out-of-policy internal prices are flagged automatically before they reach settlement

- Scenario modeling: Finance and tax teams can run what-if analysis on transfer prices before implementing changes, testing margin impact, profit allocation by entity, and potential tax exposure side by side

Vistaar's SmartPricing Suite is built for precisely this environment. It provides a single engine for internal transfer pricing management, standard discount structures, and rebate workflows.

The APIs integrate with SAP, CRM, and order-to-cash systems so that approved prices flow into execution without manual re-entry. AI/ML-based recommendations align pricing decisions with strategic objectives, and automated rebate workflows ensure that intercompany pricing is factored into total deal margin calculations.

Also Read: Navigating the AI Revolution in Pricing: Deep Dive into Strategic Implementation

How Vistaar Simplifies Transfer Pricing Management

Transfer pricing is simultaneously a compliance requirement, a margin lever, and an operational discipline. Most treat it as a compliance obligation and stop there. Prices are set by tax, documented by finance, and forgotten by the commercial teams whose order systems execute something different by quarter-end.

The enterprises getting transfer pricing right in 2026 run it through a connected pricing platform, one engine for transfer prices, rebates, and discounts, integrated into execution and monitored in real time.

Vistaar addresses the full scope of this challenge for manufacturers, distributors, and CPG enterprises:

- Complex pricing structure management: Standard discounts, internal transfer pricing, and price optimization in a single platform across entities and geographies

- Real-time price lookup: Approved transfer prices flow directly into SAP, CRM, and order-to-cash systems without manual handoffs

- AI/ML-based pricing recommendations: Decisions stay aligned with strategic objectives across both commercial and transfer pricing contexts

- Automated rebate management: Intercompany pricing is factored into the total deal and entity margin, so finance and commercial work from the same numbers

- Scenario modeling: Model the margin and compliance impact of transfer price changes before anything goes live

Schedule a demo to see how the SmartPricing Suite handles transfer pricing at scale.

Frequently Asked Questions

1. What do you mean by transfer pricing?

Transfer pricing refers to the prices set for transactions between related entities within the same corporate group. These prices determine how revenue and costs are allocated across entities and jurisdictions, which directly affects taxable income and regulatory compliance.

2. What are the 5 transfer pricing methods?

The OECD recognizes five methods: the Comparable Uncontrolled Price (CUP) method, the Resale Price method, the Cost Plus method, the Transactional Net Margin Method (TNMM), and the Profit Split method.

3. What is the arm's length principle in transfer pricing?

The arm's length principle requires that transactions between related entities be priced as if they were between independent, unrelated parties under comparable conditions. It is the global standard for transfer pricing compliance and ensures each jurisdiction collects tax on income that reflects genuine economic activity.

4. Why is transfer pricing important for manufacturers?

For manufacturers, the transfer price between production and distribution directly determines each entity's margin. Incorrect transfer prices distort divisional P&Ls, create audit exposure, and trigger double taxation.

5. How does pricing software help with transfer pricing?

Pricing software centralizes transfer price management alongside commercial pricing and rebate structures. It automates cost-plus and margin-based calculations, integrates with ERP and CRM systems via API, enforces guardrails that flag out-of-policy prices in real time, and enables scenario modeling before price changes are implemented.

As an experienced pricing solutions partner to some of the biggest names in global business, Vistaar offers a range of services to help our customers reach their maximum potential. Talk to us to see how we can help you create a more profitable future.

.png)