Key Takeaways

- An alcohol import tax is any government-imposed levy on alcoholic beverages crossing borders, including customs duties, federal excise taxes, reciprocal tariffs, state or provincial levies, and VAT/GST

- These five tax layers compound through multi-tier distribution, turning a 15% border tariff into a 25–40% shelf price increase

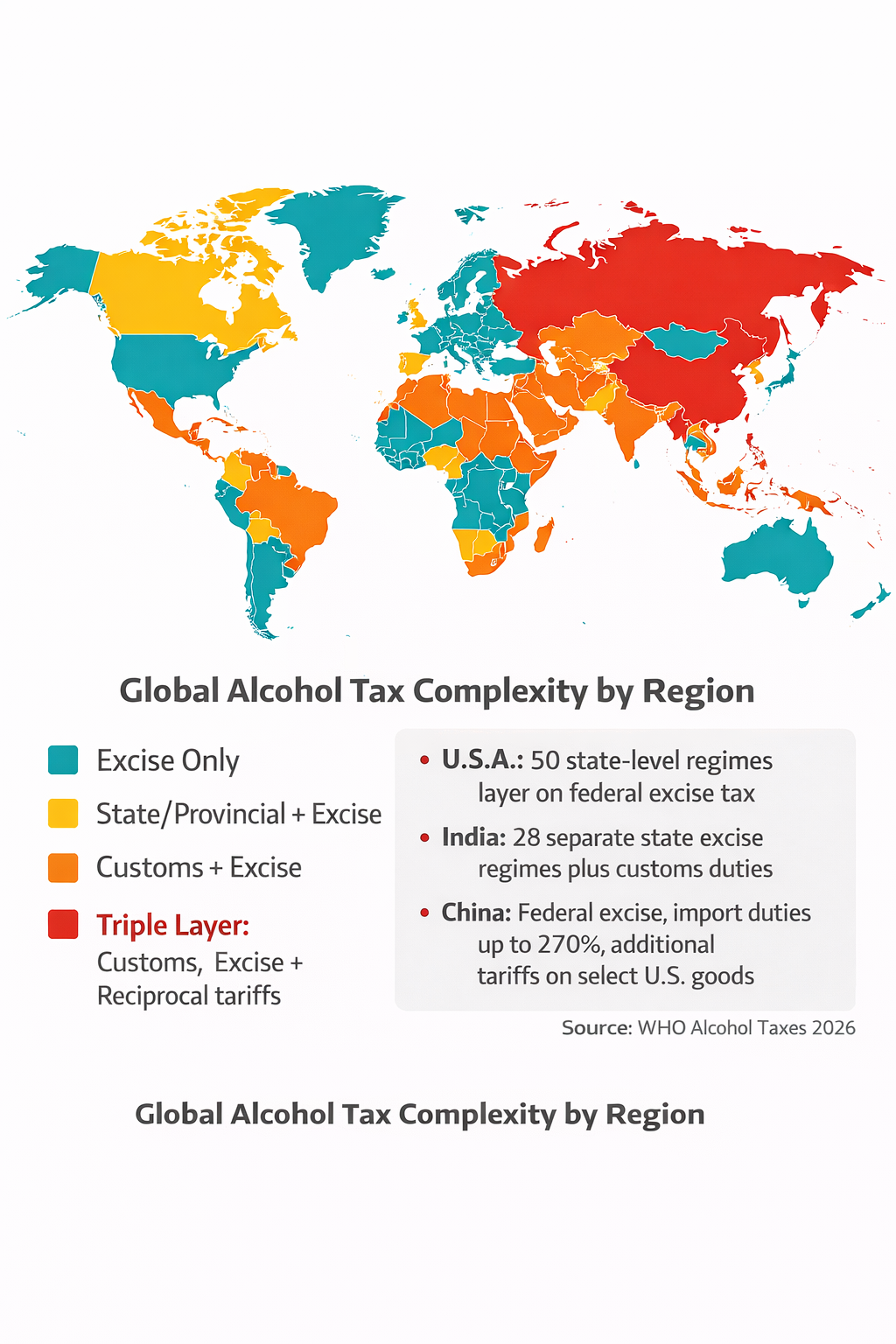

- Global tax structures vary dramatically: the U.S. has 50+ state-level regimes, India has 28+ state excise markets, 25 European countries exempt wine from excise entirely, and Canada’s provincial liquor boards control pricing and product selection

- U.S. spirits exports fell 9% in Q2 2025 and exports to Canada collapsed 85% (DISCUS)

- The execution gap between when tariffs take effect and when pricing updates reach the market is where most margin disappears. Full pass-through takes close to two years (Boston Federal Reserve)

According to the WHO’s 2025 Global Report on Alcohol Taxes, at least 167 countries apply excise taxes to alcoholic beverages. Twelve ban alcohol entirely. Twenty-five exempt wine from excise altogether. The global median excise tax share sits at just 14% for beer and 22.5% for spirits.

That is the baseline. Now layer on top of it customs duties that differ by product category and origin country. Reciprocal tariffs that change with 72 hours of notice. State-level levies that create 50 separate pricing regimes within a single country. Provincial liquor boards that can pull your brand from shelves overnight as a political response.

That is the global pricing environment for beverage alcohol in 2026.

When the U.S. imposed 25% tariffs on select European wines in 2019, French wine imports fell 54% and German wine imports dropped 42%. Those numbers were painful, but the disruption was limited to a handful of categories and one trading partner.

What followed in 2025–2026 was different in scale. Reciprocal tariffs hit 66 countries. The Supreme Court struck down the legal authority behind them. A replacement 15% surcharge took effect within days. India slashed bourbon import duties from 150% to 100%. A separate 50% tariff landed on aluminum beer cans. The EU delayed retaliatory tariffs on American whiskey, creating yet another layer of uncertainty for brands managing pricing in both directions.

For pricing teams at global beverage alcohol companies, each shift triggered a cascade of repricing decisions across hundreds of SKUs, dozens of jurisdictions, and every tier of the distribution system.

This article maps how alcohol import taxes actually work across global markets, how they cascade through distribution to amplify price impact far beyond the tariff rate, and what pricing strategies protect margin when the next change hits.

The Anatomy of Alcohol Import Taxes: What Beverage Companies Actually Pay

An alcohol import tax is any government-imposed levy applied to alcoholic beverages as they cross international borders, move through domestic distribution, or reach the point of sale. These taxes operate in five distinct layers, and for beverage alcohol, they interact with each other in ways that most industries never have to deal with.

The reason this structure matters for pricing: a tariff change at the top cascades through every layer below. If your pricing model only adjusts for the tariff itself without recalculating downstream compounding, you will underestimate margin exposure.

Layer 1: Customs duties (tariffs)

Customs duties are the first tax applied at the border when alcohol enters a country. In the U.S., these are classified under HTS Chapter 22. Rates vary by product type and origin country. For spirits, U.S. customs duties are typically assessed per proof gallon. For wine, rates depend on alcohol content and container size. Beer duties are assessed per barrel.

In other markets, customs duty structures look completely different. For example:

- India’s basic customs duty on imported liquor runs at 150% for most categories, reduced to 100% for U.S. bourbon following a February 2025 trade deal.

- Indonesia applies 90%.

- Egypt levies 1,800% on still wine and 3,000% on sparkling.

These rates determine market viability before any other pricing decision gets made.

Layer 2: Federal excise taxes

Federal excise taxes are collected at the point of import or withdrawal from a bonded warehouse. In the U.S., these differ by category: distilled spirits at $13.50 per proof gallon (standard rate), wine at rates tiered by alcohol content, and beer at $18 per barrel for the first 60,000 barrels. The Craft Beverage Modernization Act provides reduced rates for qualifying smaller producers.

In the EU, excise structures vary country by country. The UK applies a progressive duty system based on ABV. France applies relatively low excise on wine but higher rates on spirits. The Nordic countries impose some of the world’s highest excise rates on all categories.

Layer 3: Reciprocal and retaliatory tariffs

This is the layer that upended global pricing in 2025–2026. The U.S. introduced a baseline 10% universal tariff under IEEPA, later raised to country-specific rates: EU at 15%, India at 25%, South Africa at 30%, Switzerland at 39%, Canada at 35% for non-USMCA goods. After the Supreme Court struck down IEEPA tariffs in February 2026, a 15% Section 122 surcharge replaced them.

These tariffs compound on top of standard duties, creating a dual-layer border cost. A Scotch whisky entering the U.S. now faces the standard customs duty plus the 15% Section 122 surcharge, before federal or state excise taxes even apply.

Layer 4: State, provincial, and sub-national levies

This layer is where global pricing complexity becomes almost impossible to manage manually. All 50 U.S. states set their own excise rates. Washington State charges roughly $35 per gallon on spirits. Oregon, as a control state, sets prices directly. India’s state-level excise effectively creates 28+ separate markets. Canada’s provincial liquor boards (LCBO in Ontario, SAQ in Quebec) each set different markups and in some cases determine which products reach shelves. During the 2025 trade dispute, Ontario pulled American products off shelves entirely.

Layer 5: VAT/GST

In most markets outside the U.S., VAT applies at the retail level. Rates range from 5% (Japan, Canada’s GST) to 27% (Hungary). VAT is typically calculated on the tax-inclusive price, meaning it compounds on top of excise and customs duties. A 20% VAT on a price that already includes excise and tariffs amplifies every cost increase below it.

The hidden packaging tariff

Beyond the alcohol itself, a 50% tariff on imported beer in aluminum cans and empty cans took effect June 4, 2025. With 76% of U.S. packaged beer (Brewers Association) in aluminum cans and the Midwest aluminum premium at an all-time high of ~$4,800 per metric ton, this creates a cost layer that affects RTDs, canned cocktails, and craft beer.

How Global Alcohol Tax Structures Differ And Why It Matters for Pricing Strategy

A global alcohol tax structure is the full framework of taxes and duties a country applies to alcoholic beverages, including the type of tax (ad valorem, specific, or hybrid), the point of application, and the governing authority. These structures vary so dramatically across markets that a pricing model built for one country will fail in another.

This is not just a matter of different rates. Countries apply fundamentally different types of taxes, at different points in the value chain, using different calculation methods.

Ad valorem versus specific: why tax type shapes tier strategy

Some countries tax as a percentage of value (ad valorem). Others tax per unit of alcohol (specific). Many use hybrid models. Ad valorem tariffs hit premium products harder. A 15% tariff on $50 Cognac adds $7.50. The same rate on $15 vodka adds $2.25. This is why IWSR analysis identifies premium and super-premium spirits as most vulnerable to reciprocal tariffs.

Specific taxes create the opposite dynamic. A fixed $2-per-liter charge represents 20% of a $10 bottle but only 4% of a $50 bottle. For value-tier products, specific taxes compress margins disproportionately.

Market-by-market complexity

Each of these markets requires a different pricing architecture. A global pricing platform has to model these structural differences within the Gross-to-Net waterfall, not just apply flat percentage adjustments across geographies.

📖 Suggested read

For a detailed guide on building standardized pricing structures across these markets, see Vistaar’s guide on global pricing standards in beverage alcohol.

The 2025–2026 Tariff Upheaval: A Timeline and Its Pricing Impact

Between February 2025 and March 2026, the global beverage alcohol industry experienced more tariff changes than in the previous two decades combined. Each event on this timeline triggered repricing cascades across multiple markets simultaneously.

- February–March 2025:

25% tariffs on Canada and Mexico (USMCA-eligible alcohol later exempted). An additional 10% in China. 25% on all steel and aluminum. Canada retaliated with 25% on U.S. alcohol. Provincial liquor boards pulled American bourbon from shelves.

Result: U.S. spirits exports to Canada plummeted 85% in Q2 2025, falling below $10 million for the first time.

- April 2025 (“Liberation Day”):

Sweeping reciprocal tariffs on virtually all imports. Baseline 10%, China at 34%, EU at 20%. Separate 50% tariff on beer in aluminum cans. Importers froze. “The complete lack of ability to plan is crushing us,” said Dale Ott, founder of Nossa Imports, speaking to SevenFifty Daily.

- July–August 2025:

Modified rates for 66 countries. EU and Japan at 15%, India at 25%, South Africa at 30%, Switzerland at 39%. India separately reduced bourbon duty from 150% to 100%. A coalition of alcohol associations estimated 15% EU tariffs alone could result in 25,000 American job losses and $2 billion in lost sales.

- February 20, 2026:

The Supreme Court ruled 6-3 that IEEPA does not authorize tariffs. Within hours, administration invoked Section 122 with a 10% surcharge, raised to 15% the next day. EU delayed retaliatory tariffs on U.S. spirits. Section 232 tariffs on aluminum and steel remained unaffected.

The measurable impact

These numbers tell a story that extends well beyond the U.S. When Canadian provinces banned American spirits, Canadian distillers gained domestic share. When U.S. tariffs hit EU spirits, European producers redirected exports to Asian markets. When India reduced bourbon duties, Scotch producers faced new competitive pressure in the world’s largest whiskey market by volume.

Every tariff change reshapes competitive dynamics globally. The companies that respond fastest capture the opportunity. Those that take months to recalculate pricing absorb the cost.

How Alcohol Import Taxes Cascade Through the Three-Tier Pricing Waterfall

The Gross-to-Net waterfall in beverage alcohol is the pricing framework that tracks how revenue flows from initial production cost to final brand profitability. It is also the mechanism through which tariff changes amplify far beyond their nominal rate.

In the U.S. (and similar structures globally), beverage alcohol moves through a mandatory three-tier system: producers/importers, distributors, and retailers. Each tier applies a percentage-based markup. Because these markups are percentages, not flat amounts, a cost increase at the top compounds at every stage.

A 15% tariff does not create a 15% price increase at the shelf. It creates something closer to 25–40%.

An Italian amaro entering the U.S. market

The $1.50 tariff at the border became $3.25 at the shelf. That is the multiplier effect. NBER research confirms this pattern: a $1.19 tariff on a $5 wine bottle resulted in consumers paying $1.59 more. The affected categories saw a 48% decline in imports.

Where margin leaks during tariff transitions

The tariff increase is the visible cost. The less visible problem is what happens to trade programs designed around pre-tariff margins. Five failure modes create margin leakage that most pricing teams do not catch in time:

- Rebate programs on pre-tariff margins: A volume rebate consuming 8% of Gross-to-Net pre-tariff may consume 12% post-tariff, without any program terms changing

- Promotional allowances that do not auto-adjust: Trade promotions negotiated before the tariff continue at the same dollar amounts, eroding compressed margins

- Buy-downs and bill-backs at old cost bases: Distributors execute on pricing commitments made before the tariff took effect

- Price file propagation delays: Updated prices in a spreadsheet while distributors transact at stale prices

- State excise calculation lags: Compliance risk when state-level calculations do not update in sync with federal changes

“We need French, Spanish and Italian wines to make our business work,” said Harry Root of Grassroots Wine, a distributor who derives 75% of profits from European wine. “Remove any piece of the puzzle, and the whole thing doesn’t work.”

When tariffs compress those margins, the pressure cascades through the entire distribution ecosystem, including domestic brands that depend on the same network.

Five Pricing Strategies to Protect Margin When Alcohol Import Taxes Change

Knowing how tariffs cascade through the waterfall is the diagnostic step. These five strategies address specific failure modes in how pricing teams typically respond, ordered from most urgent to most strategic.

1. Pre-build tariff scenario models before changes take effect

Tariff announcements often arrive with days of lead time. The New York Federal Reserve found over 35% of manufacturers adjusted prices within a week. The companies that moved fastest had pre-modeled their scenarios. Those relying on manual analysis took months.

Pre-configured tariff scenarios that activate when changes are confirmed eliminate that lag. Vistaar’s SmartPricing and iPSM enable scenario modeling across the entire Gross-to-Net waterfall, simulating impact across every SKU, market, channel, and trade program before a tariff takes effect.

2. Calibrate absorption versus pass-through by price tier and market

Full pass-through risks volume loss. Full absorption erodes margin. The optimal response differs by price tier, by market, and by category. IWSR confirms premium and super-premium products tolerate higher pass-through. Value-tier products face elastic demand. The same logic applies across geographies: in markets with strong pricing power, higher pass-through is viable. In markets with intense local competition, absorption may be necessary.

3. Restructure rebate and trade programs around post-tariff cost bases

Rebate programs designed around pre-tariff cost structures become proportionally more expensive when tariffs increase COGS. Audit all active programs against post-tariff cost bases. Identify where rebate spend relative to margin has deteriorated. Restructure tiers, qualification thresholds, and payout rates.

Vistaar’s SmartRebate provides real-time visibility into program performance against margin, enabling rapid identification and restructuring of impacted programs.

4. Close the execution gap with real-time price propagation

McKinsey documented cases where companies delayed price changes for quarters and where a 12% cost increase went unnoticed for 14 months. In those environments, margin declines exceeded 10%.

Bain & Company research found that companies using dedicated pricing software achieve 2.5 times stronger pricing outcomes, yet only 26% of companies use pricing software. A centralized pricing engine that propagates tariff-adjusted prices to ERP, CRM, distributor portals, and e-commerce simultaneously closes this gap.

5. Model portfolio diversification across origin markets

Tariffs are origin-specific. A 15% tariff on EU spirits does not apply to New Zealand or Chile at the same rate. Brands sourcing from multiple regions can shift portfolio emphasis, but only if they can model profitability across every SKU-origin-market combination quickly. iPSM’s multi-market, multi-currency architecture enables this modeling, turning tariff volatility into a portfolio optimization input.

Navigate Global Alcohol Tax Complexity with Vistaar’s Pricing Platform

Every tariff change in the 2025–2026 cycle followed the same pattern. The rate took effect at midnight. The companies with pre-built scenario models repriced within days. Everyone else spent months catching up, and the Boston Fed data says full pass-through takes close to two years.

The margin that disappears during that gap doesn't come back.

Vistaar’s iPSM platform is purpose-built for beverage alcohol pricing complexity. Nearly 20 years of category-specific expertise. Trusted by leading global spirits and wine brands. Designed for three-tier distribution, multi-jurisdiction tax structures, excise automation, Gross-to-Net governance, and real-time price execution across markets.

What it delivers in the context of tariff challenges:

- Scenario modeling for tariff impact across the full portfolio and Gross-to-Net waterfall

- Automated excise and customs duty calculations across 50+ jurisdictions

- Real-time price propagation to distributors, retailers, and connected systems

- Rebate program analytics ensuring post-tariff margin alignment

- Multi-currency, multi-market pricing governance in a single federated platform

Clients report 1–3% margin improvement through pricing optimization and up to 5–10% margin recovery through preventive governance in beverage alcohol operations.

The next tariff change is a question of when, not whether. Find out how your pricing infrastructure would hold up before it arrives.

Request a tariff scenario assessment for your portfolio.

Frequently Asked Questions

What is an alcohol import tax?

An alcohol import tax is any government levy applied to alcoholic beverages crossing international borders. It encompasses customs duties (tariffs), federal excise taxes, reciprocal tariffs, state-level levies, and VAT/GST. These taxes stack and compound through the distribution system, meaning the consumer price impact exceeds the tariff rate itself. In the U.S. three-tier system, a 15% border tariff typically translates to a 25–40% shelf price increase.

How much is the alcohol import tax in the U.S. in 2026?

As of March 2026, imported alcohol faces a 15% Section 122 tariff (replacing IEEPA tariffs struck down by the Supreme Court), plus standard customs duties under HTS Chapter 22, plus federal excise taxes varying by category (spirits at $13.50/proof gallon standard rate, wine tiered by ABV, beer at $18/barrel), plus state excise taxes varying across all 50 states (from under $2/gallon to ~$35/gallon). Beer in aluminum cans faces an additional 50% tariff on the aluminum component.

Which alcohol categories are most affected by tariffs?

Single-origin categories legally tied to specific regions face the highest exposure because they cannot be reshored. Tequila (69% of global exports go to U.S.), Canadian whisky (79%), Cognac, Champagne, and Scotch whisky are most vulnerable. Among price tiers, premium and super-premium products are most affected by ad valorem tariffs because the tax amount scales with value. IWSR data shows these four single-origin categories accounted for roughly 70% of all spirits imports by value into the U.S.

How do tariffs differ from excise taxes on alcohol?

Tariffs (customs duties) are border taxes applied based on origin country and product classification. They are trade policy instruments. Excise taxes are internal taxes applied at production, import, or first sale, based on alcohol content, volume, or category. They are domestic revenue instruments. Both affect pricing, but they apply at different points in the supply chain, are governed by different authorities, and respond to different policy triggers.

How can beverage alcohol companies manage pricing across markets with different tax structures?

The most effective approach is a centralized pricing platform that models each market’s tax structure within the Gross-to-Net waterfall, automates excise and duty calculations, and propagates price changes in real time. This replaces manual spreadsheet processes that create lag, errors, and margin leakage during tariff transitions. Companies using dedicated pricing software achieve 2.5 times stronger pricing outcomes, according to Bain & Company research.

As an experienced pricing solutions partner to some of the biggest names in global business, Vistaar offers a range of services to help our customers reach their maximum potential. Talk to us to see how we can help you create a more profitable future.

.png)