![B2B Rebate Programs: Design, Best Practices, and Common Pitfalls [2026 Guide]](https://cdn.prod.website-files.com/6966224020021ea59eaba570/6a50ae71daf30265b269dd34_5%20-%20B2B%20Rebate%20Programs_%20Design%2C%20Best%20Practices%2C%20and%20Common%20Pitfalls%20%5B2026%20Guide%5D.png)

Key Takeaways

- Most rebate programs are expensive but unmeasured. The cost is visible on the P&L. Whether the rebate actually changed distributor behavior is rarely tracked with the same rigor.

- Rebates protect margin in ways discounts cannot: they reward actual performance rather than promised volume, and the burden of achieving the qualifying threshold sits with the buyer, not the seller.

- Flat-rate volume rebates pay for behavior that would have happened anyway. Growth-based or tiered structures that reward incremental performance above baseline are almost always more commercially efficient.

- The three leading causes of rebate program failure: designs that reward existing behavior, accrual errors from disconnected systems, and payout disputes caused by sellers and distributors working from different sales data.

Here is a question most rebate teams never ask: what would this distributor have bought without the rebate?

If the answer is roughly the same volume, the program did not generate growth. It purchased loyalty that already existed. The cost showed up on the P&L. The incremental revenue did not.

This is the fundamental problem with most B2B rebate programs. They are designed with good intentions: reward high performers, build channel relationships, drive volume. The problem is they are measured by the wrong outcomes. Total volume paid out is not the same as growth created. Distributor participation is not the same as distributor prioritization. A well-structured program and an expensive one can look identical on the surface until someone traces the payment back to its commercial impact.

For electrical distributors, rebates represent 40 to 60% of total operating profit. Without a rebate program, a competitive distribution margin often disappears entirely. This concentration makes rebate management not just a commercial optimization exercise but a business continuity concern.

What Is a B2B Rebate Program and How Does It Work?

A rebate is a post-purchase financial incentive. The buyer pays the agreed price, meets a defined performance threshold over a set period, and receives a payment (in cash, credit, or future discount) after the fact. The mechanics are straightforward. The strategy is not.

In B2B contexts, rebates serve several distinct commercial purposes, often simultaneously. Understanding which purpose a given program is actually serving is the starting point for evaluating whether it is designed correctly.

Most programs try to do several of these at once, which is where complexity grows and commercial clarity shrinks. A program designed primarily for volume concentration should look different from one designed to shift product mix. When the same rebate structure tries to do both, it typically does neither particularly well. Programs with more than three simultaneous objectives typically show materially lower distributor engagement because field reps cannot track or optimize for that many variables at once.

For a broader view of how rebates fit within channel pricing strategy, see our guide to rebate management and the specific role of channel rebates in driving distributor behavior.

Rebates vs. Discounts: What Is the Difference in B2B?

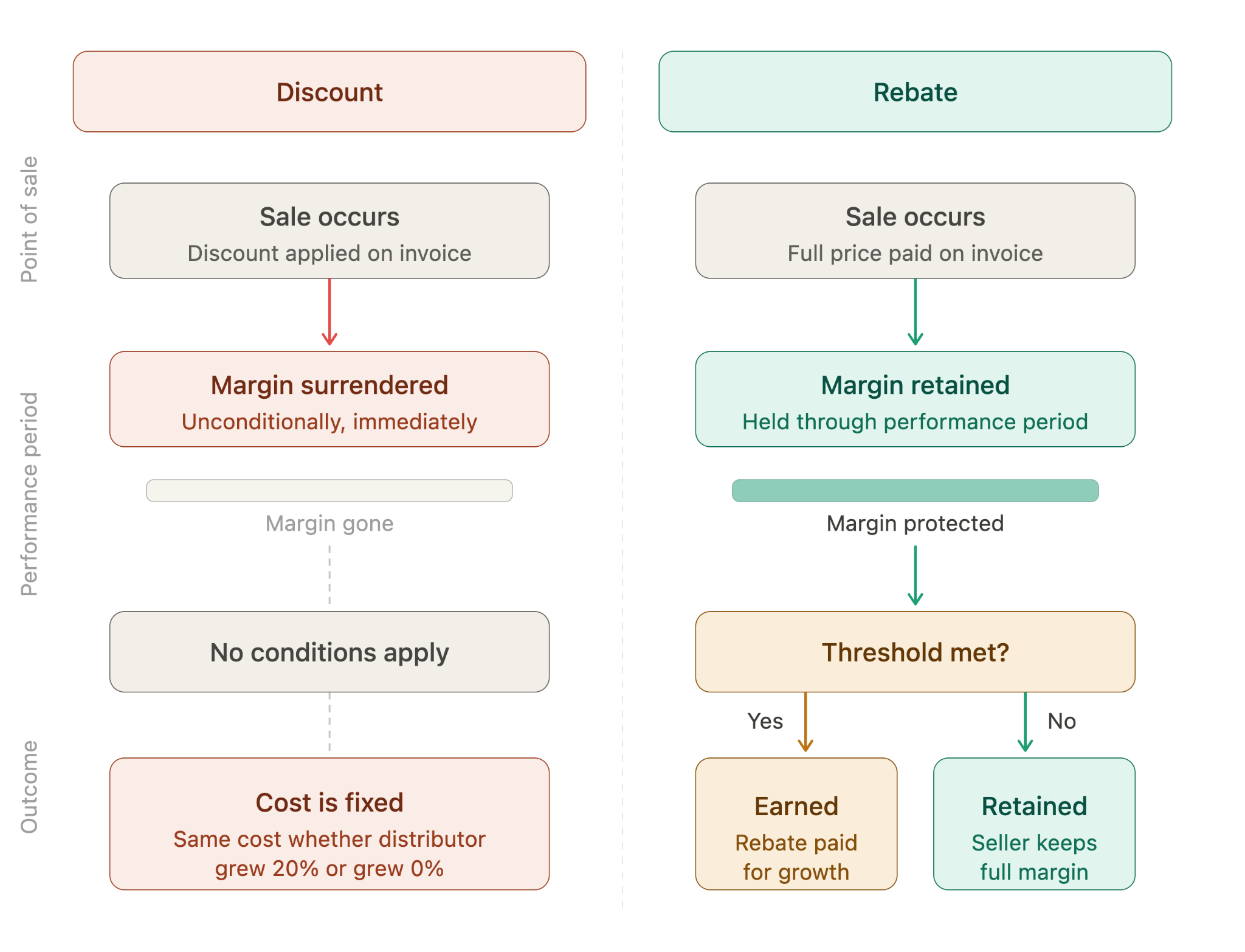

The comparison matters because rebates and discounts shape commercial behavior differently and carry different financial risk. A discount is visible to the buyer at the point of sale. It reduces the invoice price immediately and unconditionally. A rebate is conditional and retrospective: the buyer pays full price and earns the incentive only by meeting a defined performance target.

The most commercially important difference is margin protection. When a seller grants a 10% discount upfront, that margin is gone regardless of whether the distributor exceeded expectations or barely met them. A 10% rebate paid only after the distributor achieves a 15% growth target costs the same rate but only pays out if incremental performance occurs. The seller has converted a guaranteed margin concession into a conditional one.

There is also an important behavioral dynamic: discounts, when applied consistently, train buyers to expect them. They become the baseline price, and once embedded, they are nearly impossible to reverse. This is one of the reasons managing discount structures requires as much governance discipline as rebate programs. Rebates, by contrast, create a forward-looking pull: the buyer has a financial reason to keep growing with this supplier throughout the performance period, not just to place the next order at the lowest possible price.

When to use each: Rebates are better tools for volume concentration, growth incentives, product mix shifts, and long-term loyalty, meaning any situation where the commercial goal is to drive specific future behavior. Discounts are better for winning competitive deals where the decision is being made now and the immediate price is the determining factor. For businesses running everyday low pricing models, rebates tied to consistent volume rather than promotional spikes are the more natural B2B analogue.

B2B Rebate Program Examples: What Effective Programs Look Like in Practice

The difference between a rebate program that drives growth and one that funds existing behavior is best illustrated through specific cases. The following are composited from documented implementations across manufacturing and distribution.

Specialty chemicals distributor: cost-linked growth rebate

A specialty chemicals distributor serving industrial customers across three regions had run a flat-rate 2.5% volume rebate for six years. Annual payout averaged $1.8M. Growth was tracking at market rate, meaning the rebate was funding behavior that was going to happen regardless.

The manufacturer restructured to a baseline-referenced growth rebate: 0.5% on prior-year baseline volume, 4% on incremental volume above baseline, with an additional 1% kicker for distributors who grew line share by more than 3 percentage points. This kind of restructuring requires the same price optimization discipline that governs list pricing: the rates must be modeled across volume scenarios to ensure the program remains profitable even at maximum payout.

First-year results: total program cost fell to $1.4M while incremental volume above baseline grew 11%, compared to 3% market growth. The program cost less and produced more measurable growth because every dollar above the baseline payment was tied to behavior that required deliberate commercial effort.

Building materials manufacturer: the visibility effect

A building materials manufacturer managing 400+ dealer relationships ran a tiered rebate with four volume thresholds. Participation was low: fewer than 25% of dealers reached the second tier. Post-program analysis revealed that most dealers had no visibility into their current position against threshold during the performance period. They learned about their rebate at payout time, not during the months when changing their ordering behavior could have affected the outcome.

The manufacturer deployed a partner-facing performance dashboard showing each dealer their current volume, distance to the next threshold, and projected year-end payout. Within two performance periods, second-tier qualification rose from 25% to 41%. The rebate structure did not change. The visibility did. Distributors who can see they are 80% to the next threshold will push harder. Distributors who discover their position at year-end cannot.

Industrial components manufacturer: sunset provision in action

An industrial components manufacturer ran a product-mix rebate for three years aimed at shifting distributor purchasing toward a new product line. By year two, the target line had reached 30% of distributor purchases, achieving the commercial objective. By year three, the line share had stabilized at 32%, meaning the rebate was no longer changing behavior; it was simply paying for a mix that had already been established.

Because the program included a sunset clause tied to a defined commercial target (30% line share sustained for two consecutive quarters), the manufacturer was able to renegotiate the program into a lower-rate retention rebate without channel conflict. The sunset provision, written into the original agreement, made the conversation about program performance, not about taking something away. Total rebate cost fell by 40% with no measurable change in product mix.

How to Design a B2B Rebate Program That Drives Growth

Most rebate programs are built by looking at what the program paid last year and adjusting the rates. Very few are built by starting with the behavior they want to create and working backward to the structure that will create it. That difference in starting point produces almost all of the gap between programs that drive growth and programs that fund baseline purchasing.

Design around incremental behavior, not total volume

Flat-rate volume rebates, where every unit purchased by a distributor earns the same rebate rate regardless of whether volume grew, represent the most common design failure in B2B rebate programs. They reward existing purchasing patterns. The distributor who bought $2M from you last year and buys $2M again this year earns the same rebate as last year, while you have paid for growth that did not happen.

The alternative is baseline-referenced design. Define each distributor's qualifying baseline (typically prior-year purchases over the same period) and pay the full rebate rate only on volume above that line. Volume below the baseline earns either zero rebate or a significantly lower rate. The entire rebate investment is now directed at incremental behavior.

The cost difference is significant. Consider a distributor that bought $2M last year:

- Under a flat-rate 3% rebate, they earn $60,000 for maintaining the same volume. If they grow to $2.3M, they earn $69,000. You paid $60,000 for volume that was going to happen anyway and $9,000 for the $300K in incremental revenue.

- Under a growth-referenced design with 1% on baseline volume and 4% on growth above baseline, if they grow to $2.3M, they earn $20,000 on baseline + $12,000 on growth = $32,000 total. Nearly half the cost. But every dollar of rebate investment above the $20,000 baseline payment is directed at the $300K of incremental revenue you would not have had otherwise.

This structure requires more data and more administrative discipline than flat-rate programs, but the commercial return is not comparable. You are paying for growth you would not have had otherwise, not growth that was already on its way.

Common Mistake: The most expensive rebate programs are the ones nobody audited. A manufacturer adds a 2% product-mix incentive in year one, renews it automatically in year two without checking whether mix actually changed, and by year four is paying out several hundred thousand dollars annually for distributor behavior that would have happened without any incentive.

Annual reviews that trace each rebate component back to the behavior it was designed to create are not administrative overhead. They are the mechanism that prevents programs from becoming permanent margin concessions.

Make thresholds meaningful but achievable

A rebate threshold that almost no distributor reaches is not an incentive. It is a number on a contract. The same is true of a threshold set so low that nearly every distributor qualifies automatically. According to Harvard Business Review, 85% of respondents in a global survey of sales leaders believe that their pricing strategy, sales prices, discounts, and incentives need improvement. Program calibration is one of the primary reasons.

Practical calibration:

- Set tiered thresholds by distributor size. A threshold appropriate for a $50M national account will be unreachable for a $2M regional distributor. Segmenting the program by account tier allows you to challenge each segment appropriately.

- Analyze last year's distribution. If 80% of your distributors hit the highest threshold with no change in behavior, the threshold is too low. If fewer than 20% reach even the first tier, the program has no engagement. Pricing analysis at the account and segment level provides the data foundation for this calibration.

- Use growth rates, not absolute volumes. Growth-rate targets (e.g., 10% above prior year) scale naturally across distributor sizes and focus all participants on the same behavioral objective: grow faster with this supplier than with alternatives.

- Run rebate pilots before full rollout. Test new structures with top-performing or underperforming partner tiers first to see what moves the needle before committing the full program budget.

Practical Tip: Pull your last full-year rebate payout data and sort distributors into three groups: those who exceeded the highest threshold easily (threshold too low), those who fell just short (threshold well-calibrated), and those who were never close (threshold too high or wrong distributor segment).

If more than 60% fall into the first group, you are overpaying for baseline behavior. If more than 40% fall into the third group, the program has no behavioral pull. Recalibrate before renewing.

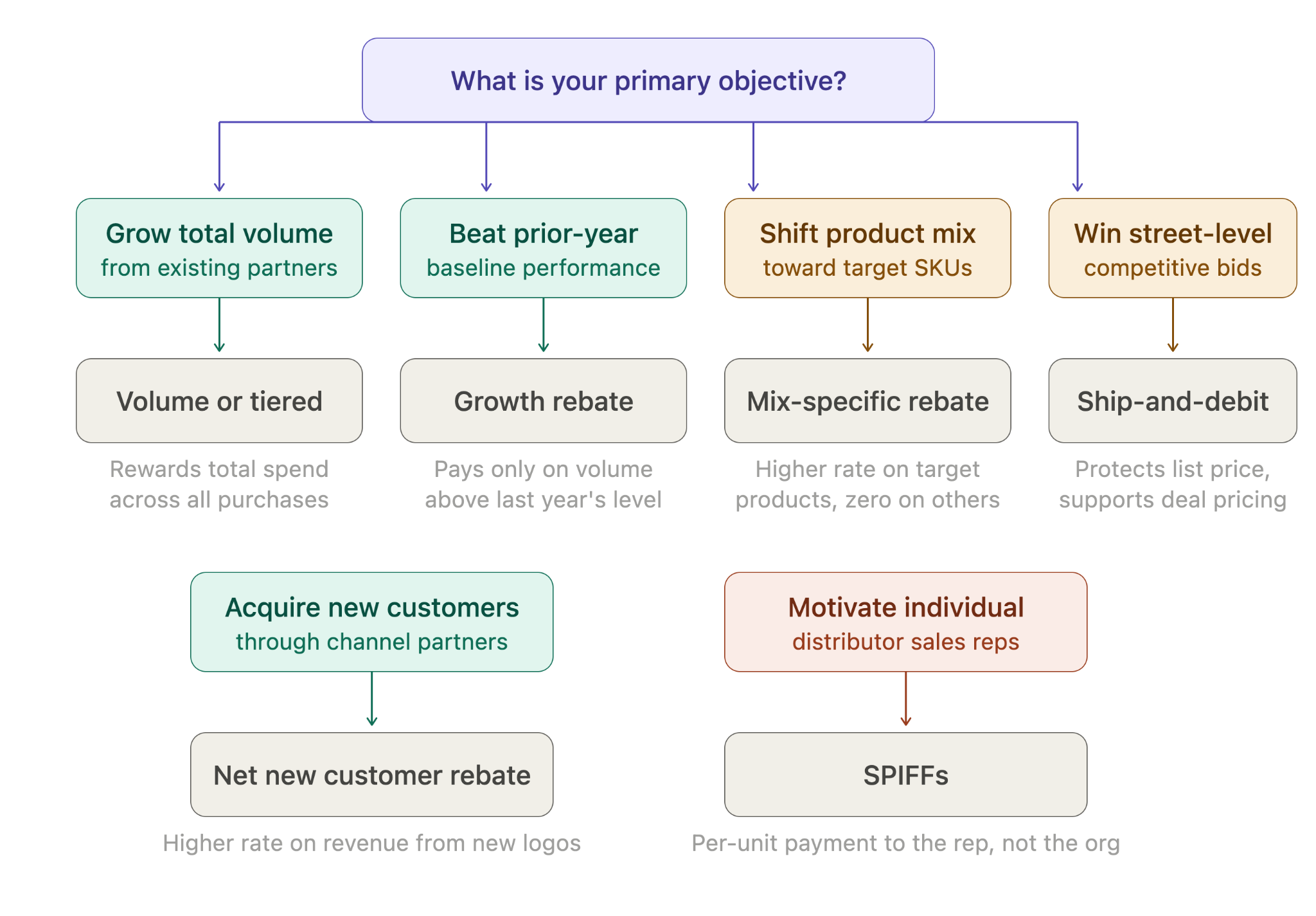

Align the rebate structure with the commercial objective

Each type of rebate structure is best suited to a specific commercial goal. Mixing structures without a clear hierarchy of objectives produces programs that are complex to administer and unclear to distributors.

SPIFFs complement account-level rebates by targeting individual rep behavior rather than organizational purchasing. A distributor may have a strong rebate incentive to sell your products, but if their reps are individually motivated to push a competitor's product through a SPIFF, your rebate investment can be undermined at the point of sale. The most effective programs align both levels.

Keep the program simple enough that distributors actually understand it

A rebate program that requires a 20-minute explanation is a rebate program that most distributors will not actively pursue. If a field sales rep cannot explain to a distributor in one sentence what they need to do to earn the highest rebate tier, the behavioral impact of the program is already compromised.

Complexity accumulates in rebate programs over time. A program starts with a clean volume structure, then someone adds a product-mix component, then a market development fund, then a loyalty payment. Each addition made commercial sense in isolation. The result is a program that finance cannot fully reconcile, sales cannot fully explain, and distributors cannot fully optimize for.

The discipline here is annual review and deliberate simplification. If a component of the rebate program cannot be linked clearly to a measurable commercial outcome, it should be questioned. Cap the number of distinct rebate structures per distributor relationship at three to four maximum. If the total number of structures exceeds what can be explained in a one-page summary, the program has likely grown beyond its own governance capacity.

Build sunset provisions into every program

Rebate programs, once established, tend to persist. Distributors build the expected payout into their pricing models, budget against it, and resist any attempt to remove it. A program that cost the manufacturer margin without producing incremental revenue in its first year gets renewed to avoid the channel conflict of canceling it.

The solution is building sunset provisions and performance review clauses into every program at inception. A program that does not meet its commercial objectives in its first full cycle should not auto-renew. This requires courage in the year-end negotiation, but it is far less expensive than funding a non-performing program for another three years.

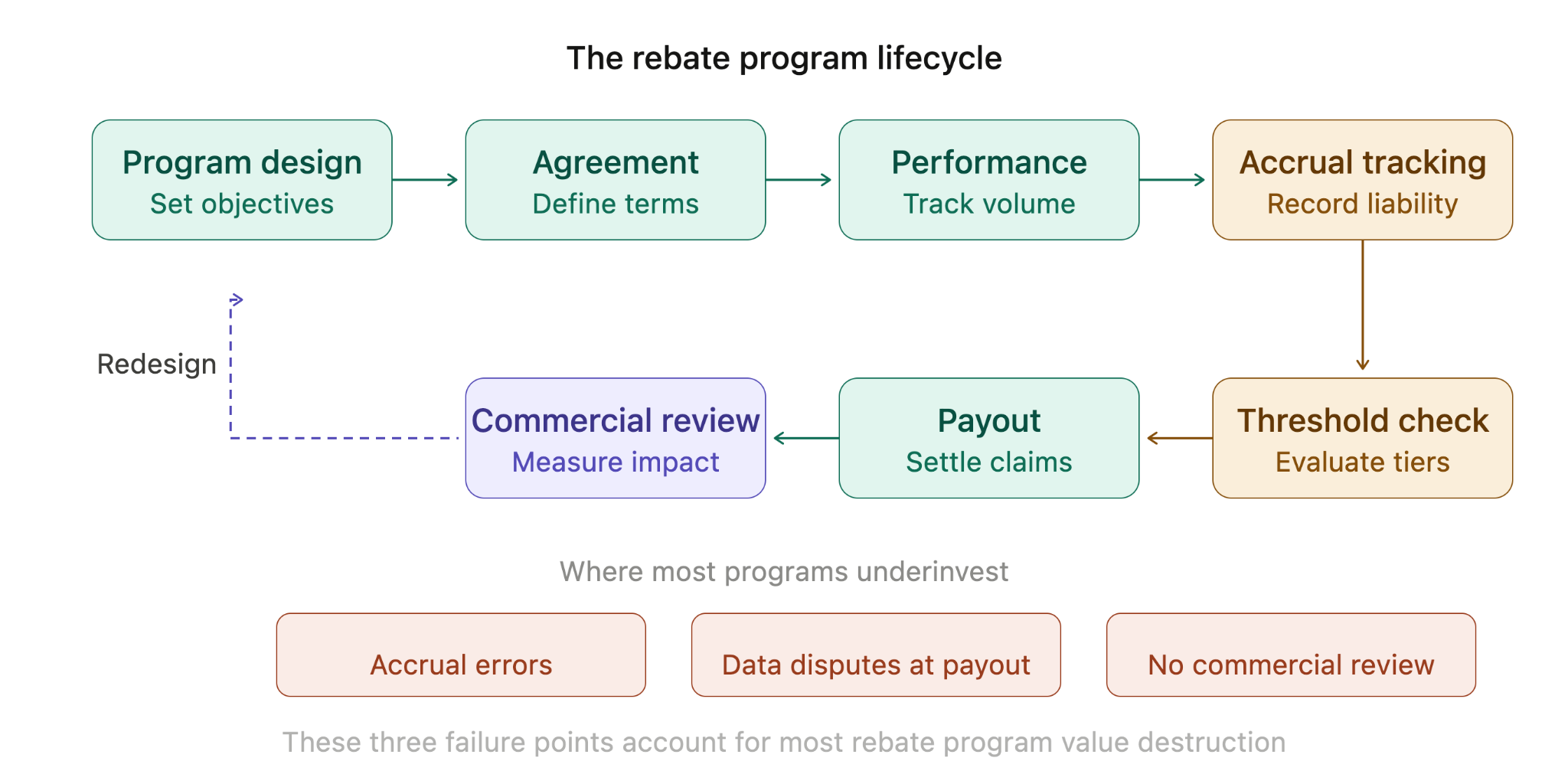

B2B Rebate Program Governance: Essential Controls, Compliance, and Technology

Governance is not documentation. It is the set of operational controls that ensure a rebate program executes as designed, pays out accurately, and can be audited when questions arise. Most rebate disputes, accrual errors, and payout surprises are governance failures, not design failures.

Define terms with commercial and accounting precision

The single most common source of rebate disputes is ambiguous program language. What counts as eligible volume? Do returns reduce the qualifying amount? Which ship-to locations are included? What happens if a distributor is acquired mid-period? What is the cutoff date for purchases to qualify for the current performance period?

These questions seem administrative until they produce a $200,000 dispute at year-end. Defining them in the program agreement upfront eliminates most of them. For businesses managing rebates alongside complex pricing strategies, these terms must also align with the broader pricing governance framework — a rebate that contradicts the logic of the list price or discount structure creates confusion for the sales team and the distributor. The standard terms that must be explicit in every rebate agreement:

- Performance period start and end dates

- Qualifying product lines, SKUs, or categories

- Eligible locations, channels, or customer types

- Treatment of returns, credits, and chargebacks

- Baseline definition and how it is calculated

- Payout timeline and payment method

- Conditions under which the program can be modified or terminated

Maintain synchronized data between seller and distributor

According to Enable's 2024 State of Volume Rebates Report, 52% of distributors do not believe they receive all the rebates they earn. The primary cause is data mismatch: the seller's sales records and the distributor's purchase records show different numbers, and neither party has a system that flags the discrepancy until claim time. Claim rejection rates of 25% or higher are common in programs where sellers and distributors are working from different data with no reconciliation process.

The operational requirement is not complicated, but it is non-negotiable: both parties must work from the same sales data, and discrepancies must be resolved in-period rather than at year-end. This means regular performance reporting shared with distributors (monthly is the standard), clear documentation of what data source governs for payout calculations, and an escalation path for disputes that does not require waiting until the performance period closes.

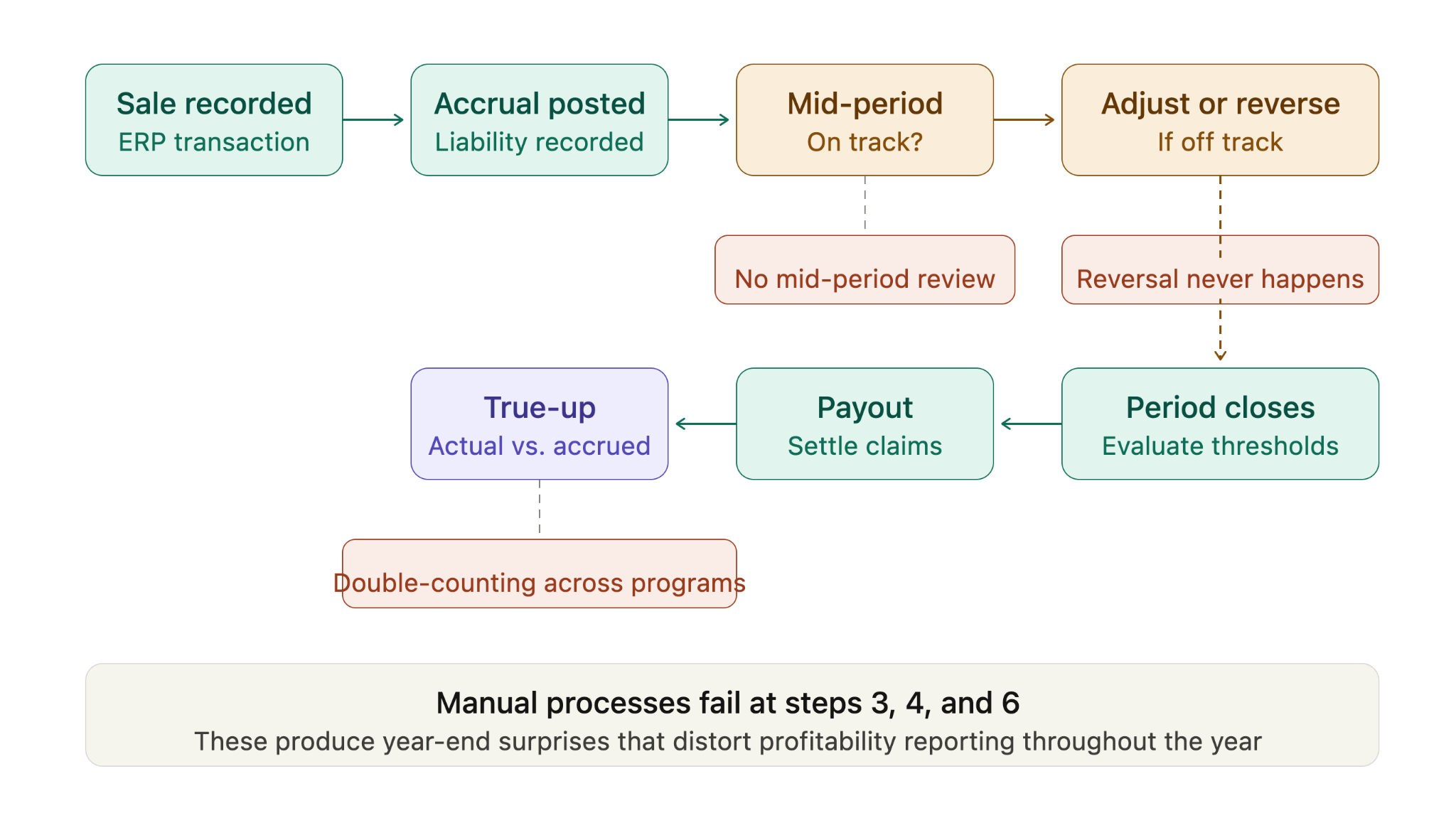

Accrue correctly and review accruals regularly

A rebate accrual is a financial liability recorded on your books before the payout occurs. It represents the rebate you expect to pay based on current performance trajectories. When accruals are wrong, the financial consequences compound: understated accruals produce surprises at year-end, overstated accruals inflate liabilities and distort profitability reporting.

Common accrual failure modes:

- Accruing on total volume instead of threshold-qualifying volume. If a distributor must reach $500K in purchases to qualify, accruing the rebate rate from the first dollar overstates the liability until the threshold is reached.

- Not reversing accruals when distributors fall short. If a distributor finishes the year below their qualifying threshold, accruals for that account must be reversed. Programs managed in spreadsheets often miss this.

- Double-accruing on overlapping programs. A distributor who qualifies for both a volume rebate and a growth rebate may generate double-counted accruals if the programs are not cross-validated. One manufacturer documented by AIMDek discovered a $175K double-payout on overlapping programs that was not caught until an annual audit.

Understand accounting compliance: ASC 606 and IFRS 15

Rebate programs carry specific accounting requirements that most commercial teams underestimate. Under ASC 606 (US GAAP) and IFRS 15 (international), rebates are treated as "variable consideration." This means they reduce the transaction price — they are not recorded as a selling expense or cost of goods sold. Revenue is recognized net of the estimated rebate from the point of sale, not when the rebate is eventually paid.

This distinction matters operationally. Finance teams must estimate rebate obligations at the time of each qualifying sale and record the corresponding liability. ASC 606 provides two estimation methods: expected value (probability-weighted outcomes across a range of scenarios) and most likely amount (the single most probable outcome). The choice of method should reflect the nature of the rebate: tiered programs with discrete thresholds typically suit the most-likely-amount method, while programs with continuous variables may suit expected value.

Three areas where auditors focus on rebate accounting:

- Estimation methodology documentation. Which method did you use and why? Is it applied consistently across similar agreements? Changing methods between periods without justification is an audit finding.

- Constraint application at the contract level. The constraint (limiting recognized revenue to amounts where a significant reversal is not probable) must be applied to individual contracts, not averaged across a portfolio. Accruing based on an average rebate rate across all customers rather than assessing each agreement separately will be flagged.

- True-up accuracy. Auditors compare prior-period estimates to actual payouts. Consistent over- or under-accrual indicates a methodology problem that requires correction.

Warning: Audit Risk

Under ASC 606, rebate accrual errors are not just operational problems, they are potential revenue misstatements. If your estimation methodology is inconsistent, if constraints are applied at portfolio level instead of contract level, or if true-up variances show a pattern of over- or under-accrual, auditors will flag it.

For manufacturers with 50+ active rebate agreements, the audit documentation burden alone often justifies purpose-built rebate management software.

Spreadsheet-based rebate tracking typically breaks down above approximately 50 active agreements. Beyond that threshold, purpose-built rebate management platforms (which automate calculation, accrual posting, and true-up reconciliation) are not just more efficient; they produce the audit-ready documentation that manual processes cannot. For more on rebate accounting requirements, see our guide to maximizing rebate accounting.

What to look for in rebate management technology

Manual rebate management: spreadsheets, email chains, disconnected ERP modules, separates the commercial agreement from the operational tracking, creating gaps where errors accumulate and disputes originate. Companies relying on legacy systems lose approximately 4 to 6% of potential profit to administrative errors and overpayments. (Computer Market Research, 2026.)

The capabilities that matter most for manufacturers and distributors managing complex channel programs:

- Centralized rebate rule management that maintains program terms, eligibility criteria, and tier structures in a single governed system rather than distributed across contract documents and spreadsheets

- Automated accrual calculation that updates liabilities in real time as transactions are recorded, reverses accruals when thresholds are not reached, and produces ASC 606-compliant documentation

- Real-time performance tracking with partner-facing visibility so distributors can see their current position against threshold and adjust behavior accordingly

- Auditable payout reconciliation that traces every payment back to the specific program terms and transaction data that generated it

- Integration with commercial pricing systems so that rebate commitments are factored into deal-level margin calculations in real time, not discovered after the fact in a quarterly reconciliation. This includes connection to competitive price intelligence feeds where rebate rates need to reflect market positioning

Automate accruals. Eliminate year-end surprises.

SmartRebate connects rebate program terms directly to transaction data, automating accrual calculations, threshold tracking, and payout reconciliation in real time. No more spreadsheet-based estimates. No more quarter-end scrambles. Every accrual is traceable, every payout is auditable, and every distributor can see where they stand.

How to Measure B2B Rebate Program Effectiveness

Most rebate programs are measured by what they paid out. Effective rebate programs are measured by what they changed. These are different questions with different answers, and only the second one tells you whether the program is generating a commercial return.

How to separate baseline from incremental growth

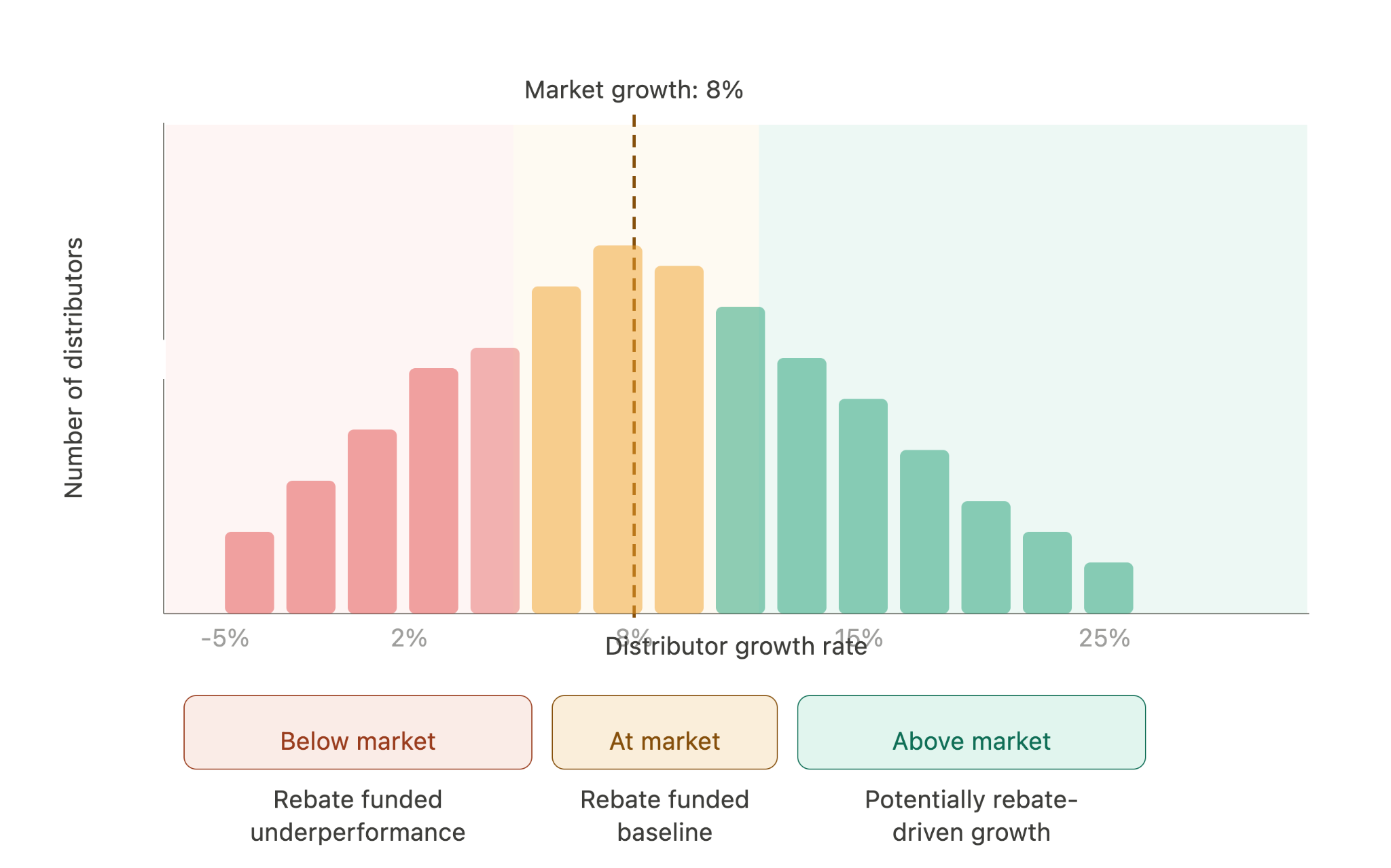

The first measurement task is establishing what each distributor would have purchased without the rebate program. This is the counterfactual baseline. Any volume above that line is potentially rebate-generated. Volume at or below that line was going to happen anyway, and the rebate payment on it is a cost without a corresponding commercial gain.

In practice, this means using prior-year performance, adjusted for market growth rates, product launches, or other known factors, as the baseline. When a distributor grows 15% while the market grows 8%, the rebate program may have contributed to roughly 7 percentage points of incremental growth. When a distributor grows 2% in a market growing 12%, the program paid for below-market performance.

The key metrics for separating baseline from incremental:

- Growth rate vs. market rate: is the distributor growing faster than the market? If not, the rebate is funding market-rate performance, not outperformance

- Line share: what percentage of the distributor's total purchases in this category go to this supplier? If line share is not increasing, the rebate is not changing purchasing mix

- Tier progression: are distributors moving up through rebate tiers over time, or clustering at the lowest qualifying level year after year?

- Program cost as a percentage of incremental revenue: the rebate investment should produce a measurable ratio of incremental revenue. If the ratio is unfavorable, the structure needs to change

- Rebate ROI by distributor tier: the same program structure can produce positive ROI with Tier 1 accounts and negative ROI with Tier 3 accounts. Measuring at the program level instead of the account level masks this

How to track the full cost of a rebate program

The rebate payment is the visible cost. The full program cost includes the administrative overhead of managing accruals and payouts, the cost of disputes and reconciliation, the finance team's time allocated to rebate accounting, and the opportunity cost of capital tied up in accrued liabilities throughout the performance period.

Organizations that implement automated rebate management systems report reducing administrative time by 50 to 70% as manual tracking and reconciliation are replaced by system-driven processes, and recovering 2 to 4% of rebate-related revenue through improved accuracy. Source: BrandMovers, B2B Rebate Management, 2026. That efficiency gain has a dollar value that belongs in the program's ROI calculation alongside the commercial impact.

Key Stat: The ROI of Rebate Automation

For a manufacturer with $500M in rebate-eligible revenue and a 3% average rebate rate, a 3% recovery on a $15M rebate budget represents $450K in annual margin recovered, before counting the administrative cost savings.

How to run an annual commercial review

Every rebate program should be reviewed annually against four questions:

- Did this program change distributor behavior? Show the performance distribution: how many distributors qualified, at what tiers, and how their growth compared to the market and to non-participating distributors

- Would the qualifying distributors have performed similarly without it? If program participants and non-participants grew at the same rate, the program is rewarding correlation, not causation

- Is the structure still aligned with the commercial objective? Markets change. A structure designed three years ago for volume concentration may now be overpaying for behavior the market has already established

- Is this program competitively necessary, or competitively differentiating? Some rebate programs exist because every competitor offers them — withdrawing would mean losing distributors. That is a retention cost, not a growth investment, and should be categorized and budgeted differently

Connecting this measurement framework to your account-level profitability data makes it possible to evaluate rebate ROI at the distributor level, not just the program level. For businesses managing pricing and rebates across the same customer base, integrating gross-to-net price waterfall analysis with rebate performance data reveals where uncoordinated rebate, discount, and contract layers are eroding margins invisibly.

The Standard for a Well-Run Rebate Program

A well-run rebate program passes a simple test: you can look at what it paid out, trace that payment to a specific behavioral change, and confirm that the commercial return exceeded the investment. Most programs fail this test because they were never designed with the test in mind.

The shift from activity-based design (reward volume, reward purchases, reward participation) to outcome-based design (reward growth above baseline, reward mix shift, reward new market development, reward net new customers) is where most of the improvement lives. It is not a technology problem. It is a commercial clarity problem.

Once the design is outcome-based, the operational requirements follow naturally: synchronized data, automated accruals, real-time performance visibility for distributors, ASC 606-compliant accounting, and annual reviews that ask commercial questions rather than just financial ones. Technology supports all of this, but it does not substitute for it.

The programs that drive genuine growth share a common attribute: someone inside the organization asked, before the program launched, what behavior this rebate will change. That question, asked consistently, separates rebate programs that build channel capability from ones that simply fund existing purchasing patterns at margin cost.

Ready to rebuild your rebate program around outcomes?

Whether you are redesigning an existing program, implementing rebate management technology for the first time, or evaluating whether your current structure is generating real growth or funding baseline behavior, Vistaar's pricing and rebate management platform gives you the infrastructure to design, govern, track, and measure rebate programs that drive measurable commercial outcomes.

Frequently Asked Questions

When should a rebate be used instead of a discount?

When the commercial goal is to drive specific future behavior rather than close the current transaction. Rebates are better tools for volume concentration, growth incentives, product mix shifts, and long-term loyalty. Discounts are better for winning competitive deals where the decision is being made now.

How do rebates work under ASC 606?

Under ASC 606, rebates are classified as variable consideration that reduces the transaction price. Revenue is recognized net of estimated rebate obligations from the point of sale, not when the rebate is paid. Finance teams must estimate rebate liabilities using either the expected value or most likely amount method, apply constraints at the contract level, and maintain documentation for audit readiness.

What is a ship-and-debit rebate?

A ship-and-debit rebate allows a distributor to sell at a competitive price below list while preserving list price integrity. The distributor invoices the customer at the lower competitive price, then submits a claim (debit) to the manufacturer for the difference between list price and the actual selling price. This structure is common in distribution markets where price competition is intense and distributors need quote-level support to win specific deals.

What is a rebate accrual?

A rebate accrual is the financial liability recorded on a seller's books representing the rebate expected to be paid based on current distributor performance trajectories. Accruals must be updated as transaction data accumulates, reversed when distributors fall short of qualifying thresholds, and reconciled against actual payouts at period end. Accurate accrual management is both an operational discipline and an ASC 606 compliance requirement.

How do you calculate a rebate?

The calculation depends on the rebate structure. For a simple volume rebate: total qualifying purchases multiplied by the applicable rebate rate equals the payout. For a tiered rebate, each volume band has its own rate. For a growth rebate, only volume above the defined baseline qualifies at the full rate. The key variables are: qualifying volume (which products, locations, and time periods count), the applicable rate at the achieved tier, and any adjustments for returns, credits, or chargebacks.

What does automated rebate management deliver?

Consistent accrual accuracy, real-time performance tracking, reduced administrative time (typically 50 to 70% reduction), fewer payout disputes, and the ability to audit every payment back to the specific program terms and transaction data that generated it.

As an experienced pricing solutions partner to some of the biggest names in global business, Vistaar offers a range of services to help our customers reach their maximum potential. Talk to us to see how we can help you create a more profitable future.

.png)